By the Numbers: Why Technical Risk is Your Construction Business's Greatest Asset in NYC

In New York City, insurance isn't just a cost of doing business—it’s often the largest line item after payroll. For small businesses, state contractors, and artisan trades, the "NYC Surcharge" is real. If you are bidding on contracts with the DEP, NYCHA, or DDC, you need to understand the data behind the risk.

Here is the 2026 outlook on the NYC commercial insurance landscape and why "just enough" coverage is a business killer.

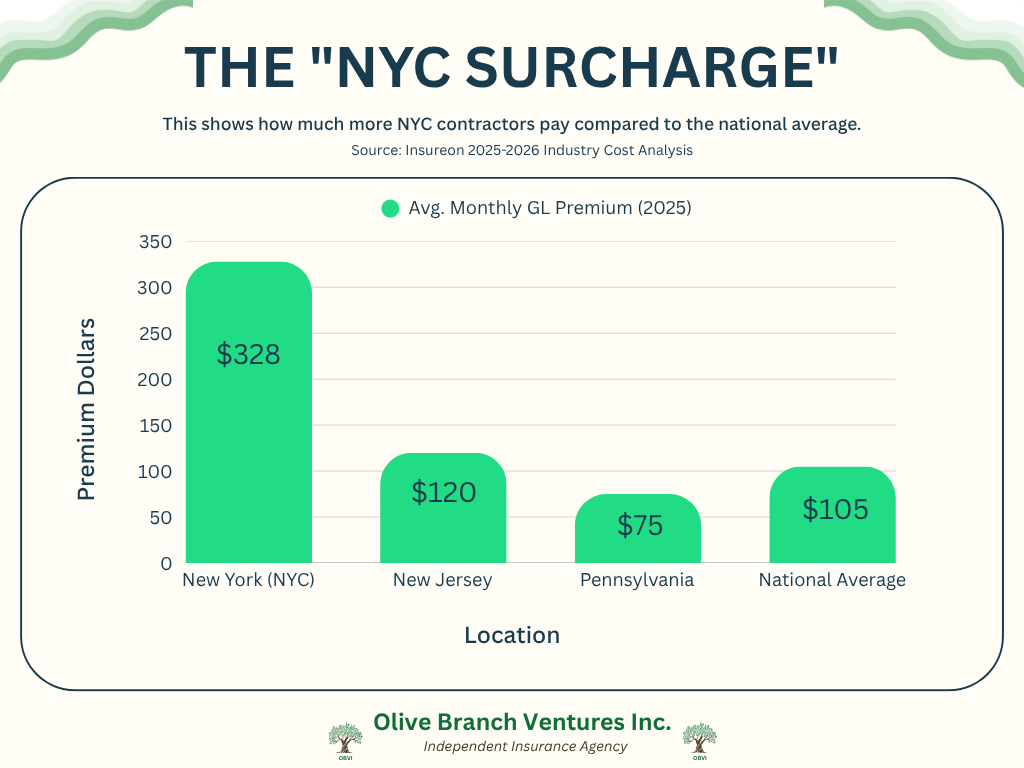

1. The "Scaffold Law" Severity Gap

New York remains the only state in the U.S. with Labor Law 240/241 (The Scaffold Law), which imposes strict liability on contractors for gravity-related injuries. Take a look at Chart 1.

The Data: In 2025, the average settlement for a Scaffold Law case in NYC reached $4.9 million. Because of this, NYC contractors pay 300% to 500% more for General Liability than contractors in neighboring states.

The Technical Risk: If your policy has a "Labor Law Exclusion," a single 6-foot ladder fall could cost you your entire business.

Source: Insureon 2025 Small Business Cost Report

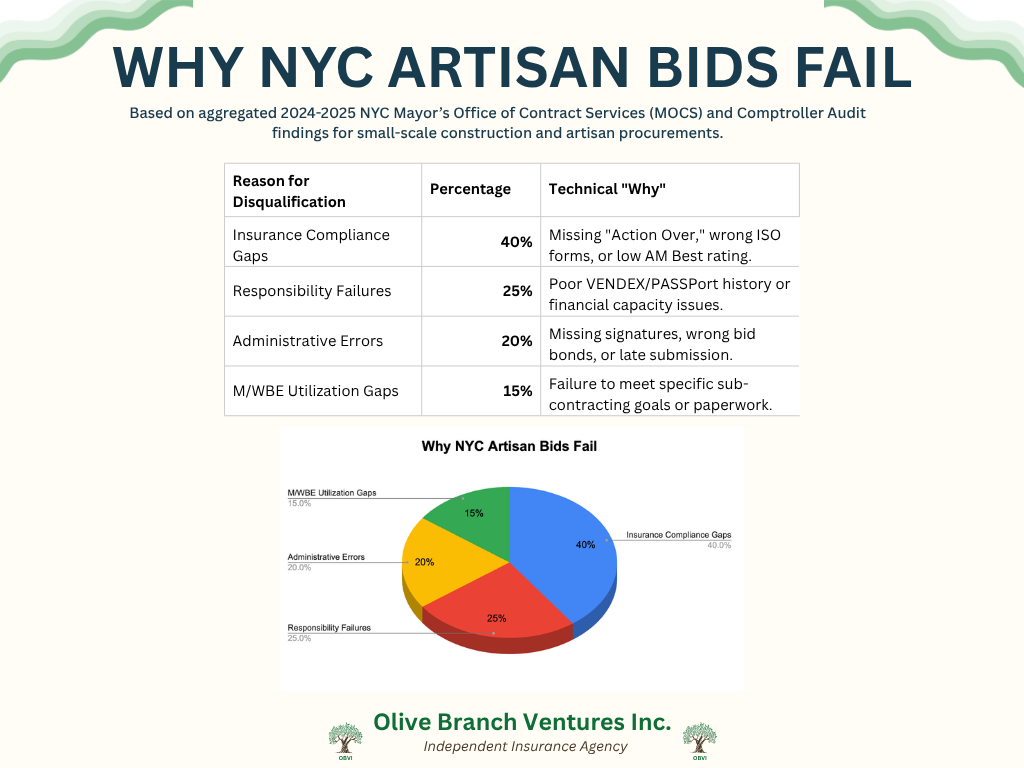

2. The 40% Disqualification Rate

You can have the best price in the world, but if your insurance paperwork is wrong, you lose the job before you even start. Take a look at Table 1.

The Data: Statistics from municipal procurement audits show that nearly 40% of artisan subcontractors (plumbers, electricians, HVAC) are disqualified from city contracts after the bid is submitted due to technical insurance errors.

Common Culprits: * Missing "Action Over" language.

An insurance carrier with a low A.M. Best rating (below A- VII).

Missing a specific Waiver of Subrogation required by the agency.

Source: NYC Mayor’s Office of Contract Services (MOCS) 2024-2025 Indicators

3. The "Silent Killer": Claim Severity vs. Frequency

A common mistake is thinking, "I’ve never had an accident, so my rates should stay low." The data says otherwise.

The Data: While job sites are getting safer (incidents are down 15% since 2020), the cost per claim has risen by over 50%.

The Impact: This is driven by "Social Inflation" and nuclear verdicts. Carriers are now requiring higher "attachment points," meaning your base policy has to work harder before your Umbrella coverage even kicks in.

Source: NCCI 2025-2026 State of the Line Report

4. The $10 Million Trap: The Umbrella Gap

Many contractors believe a $1M General Liability policy and a $10M Umbrella policy mean they are fully covered for $11M.

The Technical Reality: Our audits show a massive misalignment in "policy towers." Often, the Umbrella policy excludes the very risks (like certain heights or specific NYC vicinities) that the base GL policy covers.

The Audit Solution: A technical audit ensures your Umbrella policy sits seamlessly on top of your GL, with no "daylight" between the two that could leave you personally liable.

Conclusion: Don’t Buy a Policy, Buy an Audit

The data is clear: in NYC, insurance is not a commodity—it is a technically engineered shield. At Olive Branch Ventures, we don't just provide quotes; we provide technical audits of your "Action Over" gaps and carrier ratings to ensure you are bid-ready and fully protected.

Stop guessing at your compliance. Let’s look at your Schedule A requirements together.

#NYCConstruction #GovernmentContracts #ScheduleA #InsuranceBenchmarking #RiskManagement #ConstructionInsurance #NYCCompliance

Chart 1: NYC contractors pay 300% to 500% more for General Liability than contractors in neighboring states.

Table 1: Reasons for bid disqualification.

Data Context: Based on aggregated 2024-2025 NYC Mayor’s Office of Contract Services (MOCS) and Comptroller Audit findings for small-scale construction and artisan procurements.